How Much Are PCI Non-Compliance Fees? And How Can You Avoid Them?

Join thousands of professionals and get the latest insight on Compliance & Cybersecurity.

You open your monthly merchant statement and notice an unfamiliar fee labeled "PCI non-compliance." Your heart sinks as you see the amount—$50, $100, maybe even more—being deducted from your account. You're left wondering: Is this some kind of scam? Why am I being charged? How much will this cost me in the long run?

If this scenario sounds familiar, you're not alone. Many business owners across the country are frustrated by these seemingly arbitrary charges, with some even reporting fees as high as "$275 for annual PCI Compliance," which feels "crazy" to many merchants.

The truth is, PCI non-compliance fees are very real—and they can escalate quickly. One small business owner reported watching helplessly as their penalties started at $5,000 per month, then jumped to $25,000, before finally reaching a staggering $100,000 monthly maximum penalty that pushed them to the brink of bankruptcy.

In this comprehensive guide, we'll demystify PCI non-compliance fees, explain exactly how much they can cost your business, and provide a clear action plan to help you avoid these potentially devastating charges.

What Exactly is a PCI Non-Compliance Fee?

Before diving into the costs, let's clear up a major point of confusion: the difference between compliance fees and non-compliance fees.

A PCI compliance fee is a charge from your payment processor to cover their costs of providing a compliant service. This might include access to a portal where you can complete your compliance validation (like a questionnaire). Some merchants view these as junk fees, but they're technically for a service.

A PCI non-compliance fee is something completely different. This is a penalty charged in addition to your regular fees because you have failed to prove your compliance with the Payment Card Industry Data Security Standard (PCI DSS). This fee typically appears on monthly statements and accumulates over time if you don't address the underlying compliance issues.

Who levies these fees? The payment card networks (Visa, Mastercard, etc.) establish the requirements, but your acquiring bank or payment processor ultimately decides how much to charge you. This is why there's often a lack of transparency about the exact amounts—they can vary significantly from one processor to another.

The Staggering Cost of Non-Compliance: How Much Are the Fees?

When it comes to PCI non-compliance fees, the range is alarmingly wide. For small businesses, monthly penalties typically start between $20 to $250 per month. As one merchant noted, "I have seen these range from $20 a month to $250 a month. It really is whatever the processor decides to charge you."

But these initial fees are just the beginning. For larger merchants or prolonged non-compliance, the penalties can escalate dramatically:

- Level 1 merchants (processing over 6 million transactions annually) can face fines ranging from $5,000 to $100,000 per month.

- For severe violations or extended periods of non-compliance, penalties can reach up to $500,000.

The real-world impact is sobering. One business owner shared their harrowing experience on Reddit: "They're getting hit with $100,000 monthly penalties from their acquirer. Started at $5,000/month, escalated to $25,000, now at the maximum penalty tier." This escalation pattern illustrates how quickly these fees can become existential threats to your business.

Several factors influence the exact amount you'll be charged:

- Transaction Volume: Your PCI Compliance Level determines the baseline for potential penalties.

- Duration of Non-Compliance: The longer you remain non-compliant, the higher the monthly penalty. A Level 1 company non-compliant for over 7 months can face the maximum fines of $100,000 per month.

- Your Payment Processor: Different processors have different fee structures, which is why shopping around can sometimes help you find better terms.

The Hidden Costs: Why Fines Are Just the Tip of the Iceberg

While the direct non-compliance fees are substantial, they pale in comparison to the potential costs of a data breach—which becomes significantly more likely when you're not PCI compliant.

According to the Ponemon Institute, the average cost is $150 per compromised record in a data breach. For a small business with just 1,000 customer records, that's a potential $150,000 hit. You can even use their Data Breach Cost Calculator to estimate your specific risk.

Additional breach-related costs include:

- Card Replacement Fees: $3-$10 per compromised card

- Forensic Investigations: To determine the cause and extent of the breach

- Increased Processing Rates: Higher fees for future transactions

- Potential Termination: Your merchant account could be shut down entirely

The legal and reputational damage can be even more devastating. Consider these high-profile examples:

- TJX Companies suffered a breach in 2007 affecting 100 million cards, resulting in a $40.9 million settlement.

- Target's 2013 breach led to $18.4 million in penalties and a staggering $440 million loss in revenue in the following quarter.

As one Reddit user bluntly put it: "Ignoring compliance warnings leads to severe financial penalties and potential bankruptcy."

Are You at Risk? Understanding PCI Compliance Levels

Your specific compliance requirements—and consequently, your potential non-compliance fees—depend on your merchant level. There are four levels of PCI compliance based on annual transaction volume:

Level 1: Merchants processing over 6 million card transactions annually.

- Requirements: Annual Report on Compliance (ROC) by a Qualified Security Assessor (QSA)

- Potential Monthly Penalties: Up to $100,000

Level 2: Merchants processing 1 to 6 million transactions annually.

- Requirements: Annual Self-Assessment Questionnaire (SAQ) and quarterly network scans

- Potential Monthly Penalties: $25,000 to $50,000

Level 3: Merchants processing 20,000 to 1 million e-commerce transactions annually.

- Requirements: Annual SAQ and quarterly network scans

- Potential Monthly Penalties: $10,000 to $25,000

Level 4: Merchants processing fewer than 20,000 e-commerce transactions annually, or up to 1 million regular transactions.

- Requirements: Annual SAQ and possibly quarterly scans

- Potential Monthly Penalties: $5,000 to $10,000

Most small businesses fall into Level 4, but don't let that lull you into a false sense of security. The penalties at this level can still be devastating for a small operation.

Your Action Plan: A Step-by-Step Guide to Avoiding PCI Non-Compliance Fees

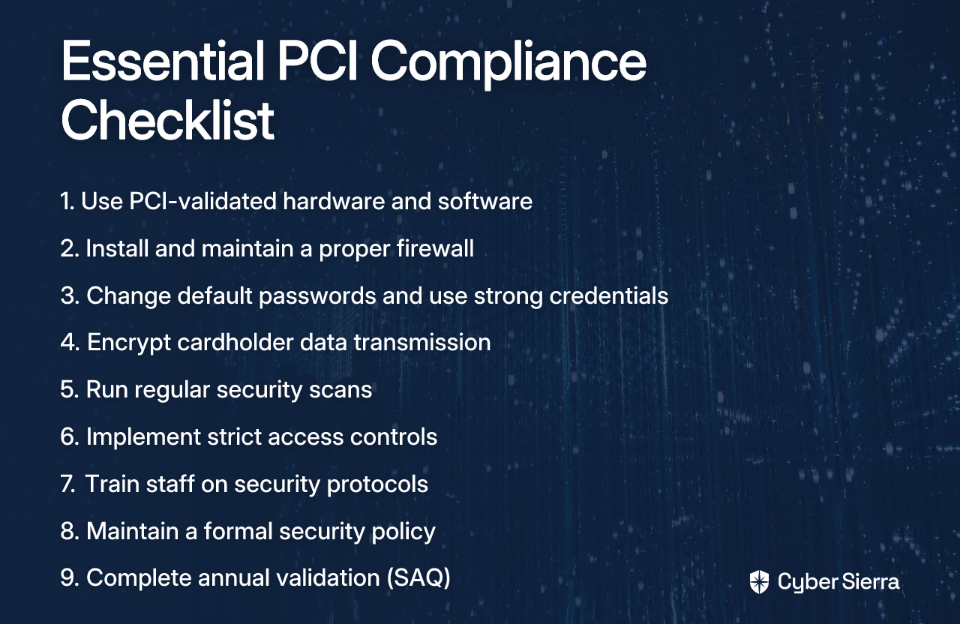

The good news is that becoming PCI compliant is completely achievable with the right approach. Here's a comprehensive checklist to help you avoid those costly non-compliance fees:

1. Use Approved Hardware and Software

Ensure your POS systems, card readers, and payment software are PCI-validated. Using non-compliant equipment is one of the quickest ways to fail your compliance validation.

2. Install and Maintain a Firewall

A properly configured firewall is your first line of defense against unauthorized access to your network and cardholder data environment.

3. Secure Your Systems

- Change All Default Passwords: Never use vendor-supplied default passwords or security parameters.

- Use Strong, Unique Passwords: Implement robust password policies for all system access.

4. Protect Cardholder Data

- Encrypt Transmission: All cardholder data transmitted across open, public networks must be encrypted.

- Avoid Storing Sensitive Data: Never store the full magnetic stripe data, card validation code (CVV), or PIN data. Limit storage of any cardholder data to only what is absolutely necessary.

5. Maintain a Vulnerability Management Program

- Use and Regularly Update Antivirus Software: Protect all systems against malware and viruses.

- Conduct Regular Security Scans: Perform quarterly network vulnerability scans (a control scan) with an Approved Scanning Vendor (ASV) if required for your level.

6. Implement Strong Access Control Measures

- Restrict Access: Limit physical and system access to cardholder data on a need-to-know basis.

- Assign Unique IDs: Give each person with computer access their own unique ID to ensure accountability.

7. Train Your Staff

Regularly educate all employees on security protocols and the importance of protecting cardholder data. Human error is a leading cause of security breaches and fraud.

8. Maintain an Information Security Policy

Create and enforce a policy that addresses information security for all personnel.

9. Complete Your Annual Validation

For most small businesses (Level 4), this means completing the annual PCI DSS Self-Assessment Questionnaire (SAQ). For more information on the SAQ, see What is PCI SAQ?.

"I've Been Charged a Fee! What Do I Do Now?"

If you've already been hit with a PCI non-compliance fee, don't panic—but don't ignore it either. Here's what to do:

Step 1: Don't Ignore It

The problem will only get worse and more expensive. As one business owner warned, ignoring compliance warnings can lead to "severe financial penalties and potential bankruptcy."

Step 2: Contact Your Processor Immediately

Call your merchant services provider right away. Ask what specific steps are needed to become compliant and have the fee removed. Often, simply completing your SAQ is enough to stop the penalty from recurring.

Step 3: Negotiate or Switch

- Ask your processor if they're willing to waive the fee once you become compliant.

- If your processor is inflexible, remember that "it may not be optional with your current provider, but with other providers it is either $0 or close to it." Compare offers from different payment processors to find better terms.

Compliance Isn't a Cost, It's an Investment

PCI compliance may seem like an administrative burden, but it's actually a critical investment in your business's security and longevity. The potential costs of non-compliance—from the direct fees ($5,000 to $100,000+ per month) to the devastating impact of a data breach—far outweigh the effort required to maintain compliance.

As one industry expert put it, the new PCI DSS 4.0 requirements "aren't suggestions—they're business survival requirements." In today's digital economy, protecting your customers' data is not just the right thing to do—it's essential to protecting your business's bottom line and reputation.

Take action today by using the checklist provided to assess your compliance status. For a comprehensive overview of all requirements, visit the official PCI Security Standards Council website. Your business's future may depend on it.

Frequently Asked Questions

What is a PCI non-compliance fee?

A PCI non-compliance fee is a monthly penalty charged by your payment processor or acquiring bank when your business has not proven its compliance with the Payment Card Industry Data Security Standard (PCI DSS). Unlike a standard compliance fee which covers the cost of compliance tools, this is a punitive charge that can accumulate over time if the compliance issues are not resolved.

Why am I being charged a PCI non-compliance fee?

You are being charged a PCI non-compliance fee because you have failed to demonstrate that your business meets the required PCI DSS security standards. This typically happens when you do not complete and submit your annual validation documents, such as the Self-Assessment Questionnaire (SAQ), or fail to address security vulnerabilities identified during required scans.

How much can PCI non-compliance fees cost my business?

The cost of PCI non-compliance fees varies widely, ranging from $20 to $250 per month for small businesses. For larger merchants or for prolonged periods of non-compliance, these penalties can escalate dramatically, reaching from $5,000 to as high as $100,000 per month for Level 1 merchants.

How can I avoid PCI non-compliance fees?

The most effective way to avoid PCI non-compliance fees is to achieve and maintain PCI DSS compliance. This involves using approved hardware and software, securing your systems with firewalls and strong passwords, protecting cardholder data through encryption, regularly scanning for vulnerabilities, and completing your annual compliance validation, such as the Self-Assessment Questionnaire (SAQ).

What should I do if I've already been charged a non-compliance fee?

If you have been charged a non-compliance fee, you must act immediately. Contact your payment processor to understand the specific steps needed to become compliant. Complete any required actions, such as submitting your SAQ, and then ask your processor if they will waive the fee. If they are unwilling to work with you, consider comparing offers from other providers.

Is PCI compliance mandatory?

While PCI DSS is not a federal law, it is a contractual requirement mandated by the major payment card brands (Visa, Mastercard, American Express, etc.). If you want to accept card payments from these brands, you are contractually obligated to be compliant. Failure to comply can result in fines, increased transaction fees, or even the termination of your merchant account.